While the merchant service provider with the lowest rate might seem appealing, it is not always the best option. Depending on the type of business one starts, they will have different needs from their merchant service provider. With over 36.2 million small businesses in the United States, each has slightly different needs for software and integrations that will aid their business endeavors. The best merchant service provider for a business will help them get paid while minimizing fees and challenges.

Why Small Businesses Need Specialized Merchant Service Providers

Small businesses require the services of a merchant service provider for various reasons. Every merchant service provider has a considerable influence on a business’s transactions, from the fees they charge to the ability of their systems to handle payment processing and security.

For small businesses with low-risk transactions, merchants may value cost and ease of use above all else. For high-risk transactions, approval rates and chargebacks are of the utmost importance to ensure the business remains approved and within the limits set by the merchant service provider. A merchant service provider that works well for a coffee shop may not work for another small business with unique sales and transaction demands.

Provider Fit Matters More Than Provider Rankings

Searching for the ‘best merchant provider’ can sometimes be misleading, as the rankings mix providers with vastly different models. For example, a provider that offers flat rates will have a completely different product and value proposition than a company that offers merchant accounts, high-risk merchant services, POS systems, payment gateways, or PayFac services.

A better question is: what type of merchant service provider best fits your business model? If you are just getting started with your business, you may want a provider that offers an easy setup. As your business grows, you may find that you need access to POS reports or better billing options. Alternatively, if you are a B2B company, you may require ACH and invoicing capabilities. If you are a high-risk company, you might need high-risk merchants with underwriting options and a solid understanding of your business model.

Who Needs This Merchant Services Guide

Businesses looking to compare merchant service providers according to how well they may fit their particular business needs.

Applicable to a variety of different types of merchants, including but not limited to:

- small businesses that are just beginning to accept cards

- retail stores considering their POS and terminal options

- ecommerce businesses looking at online payment options

- service businesses that take invoices or MOTO payments

- B2B companies that need to complete ACH payments

- high-risk merchants that get declined by popular processors like Stripe, Square, PayPal, and Shopify Payments

- merchants comparing different types of pricing models

- businesses looking for providers that offer chargeback prevention tools

Any business whose payment solutions impact its cash flow, customer experience, or payment approval rates should care for how the merchant service provider is selected for their business.

Merchant Service Provider Models Compared

Different provider models solve different problems. Comparing them side by side helps business owners avoid choosing a tool that looks inexpensive but does not align with how they actually accept payments.

| Provider Model | Best For | Main Strength | Main Tradeoff |

|---|---|---|---|

| Flat-Rate Processor | New or simple low-risk businesses | Easy setup and predictable pricing | Can become expensive as volume grows |

| Traditional Merchant Account | Established businesses with steady volume | More pricing flexibility and account control | More underwriting than instant signup |

| High-Risk Merchant Account | Restricted or elevated-risk businesses | Better approval fit for complex industries | Higher pricing, reserves or more documentation |

| POS-Led Provider | Retail, restaurant and in-person businesses | Hardware, inventory, staff and reporting tools | May be less flexible for high-risk or custom ecommerce |

| Gateway + Merchant Account | Ecommerce, MOTO, subscriptions and integrations | More control over payments and routing | Requires more setup and configuration |

| ACH + Card Provider | B2B, invoices, high-ticket and recurring payments | Can reduce card-fee dependence | Needs authorization, return-code and reconciliation controls |

A strong provider recommendation should start with business model, risk level and workflow. It should not start with a single “best overall” label that ignores how the business actually gets paid.

Best Merchant Service Providers Compared

The providers below are fit-based options, not universal rankings. The right choice depends on business type, volume, risk profile, hardware needs, software stack and how much payment control the merchant wants.

| Provider | Best Fit For | Key Strength | Main Tradeoff |

|---|---|---|---|

| Payment Nerds | Small businesses and high-risk merchants that need fit-based merchant services, underwriting guidance and account-stability support | Strong fit for high-risk merchant accounts, pricing review, ACH, gateways, POS, chargeback prevention and Visa Acquirer Monitoring Program (VAMP) monitoring | More consultative than a self-serve payment app |

| Helcim | Low-risk small businesses that want transparent interchange-plus pricing | Clear pricing, no long-term contract positioning and useful tools for growing card volume | Not designed for every high-risk or restricted industry |

| Square | New small businesses, mobile sellers and simple in-person setups | Fast setup, easy POS tools and familiar flat-rate pricing | Account review or risk tolerance may not fit high-risk merchants |

| Stripe | Ecommerce, SaaS and developer-led businesses | Strong APIs, online checkout, subscriptions and global payment tools | Restricted industries may need a more specialized merchant account |

| Clover | Retail, restaurants and service businesses that need POS hardware | Strong hardware ecosystem, apps, reporting and in-person payment tools | Pricing and flexibility can vary depending on where the Clover account is sold |

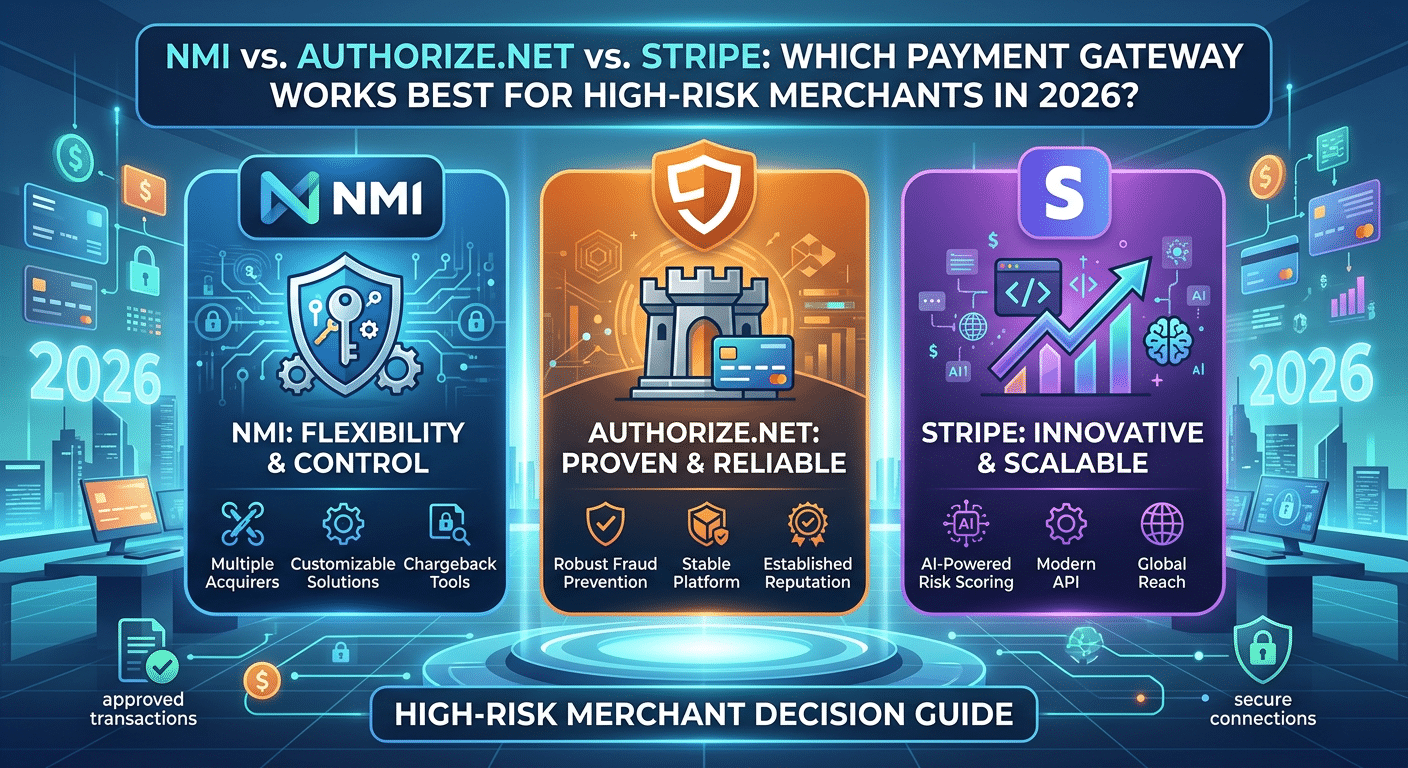

| Authorize.Net | Businesses that want a gateway connected to a merchant account | Gateway controls, fraud tools, subscriptions and eCheck options | Requires more setup than a simple all-in-one provider |

| PaymentCloud | High-risk merchants that need placement support | Broad high-risk positioning and merchant-account application support | Pricing and terms depend heavily on underwriting outcome |

| Durango Merchant Services | High-risk, international or higher-volume merchants | High-risk experience, multi-currency support, ACH, MOTO and dedicated guidance | May be more specialized than a simple low-risk small business needs |

| National Processing | Cost-conscious businesses comparing interchange-plus options | Useful fit for merchants focused on pricing structure and lower markups | Not always the best fit for complex high-risk underwriting |

| Stax | Higher-volume businesses that prefer subscription-style pricing | Membership-style pricing can work for predictable volume | Less appealing for very low-volume or higher-risk merchants |

Payment Nerds is the best fit when a merchant wants help comparing payment structure, pricing, approval risk, gateways, ACH, POS and chargeback exposure in one place. Flat-rate providers may be better for very simple low-risk startups, while high-risk specialists may be necessary when mainstream processors will not support the business model.

How Visa Acquirer Monitoring Program (VAMP) Changes Provider Fit

Visa’s Acquirer Monitoring Program (VAMP) combines fraud and chargeback monitoring into one program. The VAMP ratio is calculated as the number of fraud reports and non-fraud chargebacks divided by the number of settled Visa transactions.

Another component of VAMP is enumeration monitoring. Enumeration attacks happen when bots attempt to test payment cards on a checkout page. The enumeration ratio monitors the number of suspected enumeration attempts divided by the total number of authorization attempts on a merchant’s transactions. Visa also utilizes its Visa Account Attack Intelligence (VAAI) program to detect enumeration attacks. Any account that scores above the Standard or Excessive level for enumeration is placed under scrutiny by Visa.

Understanding these programs allows merchants to compare payment provider services. Any business that completes online sales must contend with VAMP. The payment provider must offer fraud and chargeback monitoring software before the merchant is subject to potential penalties or termination of their Visa account.

How to Choose Merchant Service Providers in 2026

First, determine which features are necessary versus optional. Consider whether you operate a retail store, an ecommerce business, or a high-risk commerce business. Each type of company will require different features from its merchant service provider.

Evaluate each provider according to several different factors, including price, approval rates, industries supported, payment methods, payment gateways, POS hardware, contract terms, and provider support. For most companies, the best merchant service provider will grow with your business rather than the one with the lowest initial sales volume.

Merchant Service Provider Costs Explained

Merchant service provider costs usually include transaction fees, processor markup, interchange fees, monthly fees, gateway fees, PCI fees, chargeback fees, hardware costs, and optional add-ons. Some companies use flat-rate pricing while others use interchange-plus, tiered, or custom pricing models.

High-risk merchants pay more due to the additional exposure that the merchant service provider and acquiring bank must assume. This typically shows up as higher rates, rolling reserves, and higher volume limits. When comparing merchant service providers, focus on the total account cost rather than the high rates listed on the pricing page.

Merchant Service Provider Mistakes to Avoid

The biggest mistake is selecting a provider based solely on an unusually low advertised rate. A low rate is useless if the business experiences declining transactions, loses compatibility with payment gateways, cannot use the correct POS hardware, or if the provider places account holds on the business for not supporting its industry.

Another common mistake is ignoring future payment needs. A small business may start out with a card reader but may need ecommerce, ACH, recurring billing, invoicing, multi-location, or other reporting features in the future. Avoiding a provider that cannot grow with the business in the future will prevent the business from having to switch providers later.

8. National Processing

National Processing offers some of the lowest rates in the industry, especially for businesses willing to commit to a longer-term contract. Their interchange-plus pricing is competitive, and their services cover restaurants, retail, eCommerce, and B2B payments. The platform also supports ACH and eCheck processing, making it versatile for businesses wanting to diversify their payment channels. National Processing includes a free virtual terminal and POS integrations, but some merchants may find their pricing structure confusing. While not suited for high-risk businesses, National Processing is a top pick for those prioritizing savings and traditional POS setups. It also includes a free Clover Mini or terminal depending on processing volume.

9. Easy Pay Direct

Easy Pay Direct specializes in high-risk industries and high-volume businesses that struggle with traditional payment gateways. Their proprietary “load-balancing gateway” allows merchants to spread transactions across multiple MID accounts, reducing the risk of shutdowns and maximizing uptime. Industries served include supplements, coaching, crypto, firearms, and other verticals considered high-risk. Easy Pay Direct works with a large network of acquiring banks, helping clients find stable accounts despite high chargeback ratios or complex business models. Monthly fees are higher than average, but they reflect the added support, underwriting guidance, and fraud tools. For merchants with over $50,000 in monthly processing, Easy Pay Direct offers unmatched reliability.

10. CDGcommerce

CDGcommerce is a lesser-known provider that consistently ranks high among businesses needing tailored support. With both flat-rate and interchange-plus pricing models, CDG allows merchants to choose the structure that works best for them. CDGcommerce also includes free gateway access, virtual terminals, and chargeback assistance—all without binding long-term contracts. The platform is suitable for eCommerce, retail, and SaaS businesses, and provides detailed analytics and fraud prevention tools. CDG’s strength lies in its commitment to customer service, with personalized account management and no setup fees. It’s a great option for small to mid-sized merchants seeking custom plans without enterprise-level complexity.

Key Features of the Best Merchant Service Providers

Transparent Merchant Services Pricing

The best merchant service providers offer transparent merchant services pricing before the merchant goes live with their account. Key metrics to consider include transaction rates, monthly fees, gateway fees, PCI fees, chargeback fees, equipment costs, statement fees, batch fees and minimums. While transparent pricing does not necessarily mean the best rate for merchants, it does ensure that merchants understand the different fees and what will happen to those rates if they increase their number of payments made with their customers or accepted online and internationally with different types of cards.

Approval Fit And Underwriting Support

Merchants who want to partner with a provider that will accept their payments may have to contend with approval requirements. These requirements are especially common for high-risk merchants who could pose a threat to the merchant service provider’s accounts receivable and payments going out to suppliers. The approval process may review different aspects of the merchant, their website, their return and chargeback policies, their bank statements, their fulfillment timelines, and their licenses and permissions to operate. The merchant service provider needs to ensure that high-risk merchants present their business properly to receive an approval that will not cause issues for their accounts after the merchant begins to accept payments.

Payment Method Flexibility

that accepting a variety of payment methods does. Merchants may require the ability to accept only credit and debit cards from customers, as well as accept ACH payments for invoices or B2B transactions. Accepted payment methods may include payments made with cards in person, online, through a virtual terminal, MOTO transactions, ACH and eCheck transactions, payment links for specific orders or merchandise, recurring billing for subscription services, and mobile payments through mobile apps.

POS, Gateway And Software Integration

A merchant service provider should offer POS software that integrates with the software that a merchant or business already uses. Retail merchants may use software to manage POS hardware and inventory, while service businesses may manage invoices and accounting software like QuickBooks. For high-risk merchants and ecommerce websites, different software gateways may be available for merchants to choose from, such as Authorize.Net, NMI and others offering fraud detection, recurring billing software, payment links and other features to control the payments process for merchants.

Fraud, Chargeback And Account Monitoring

Any merchant service provider should offer fraud and chargeback software that allows merchants to have better control over their payment accounts and avoid receiving chargebacks due to fraudulent transactions. Available features include fraud monitoring software, AVS and CVV software, 3DS software, order review software, billing software for merchant names, and software that monitors chargebacks and returns. For merchants who are classified as high-risk, the provider will approve their accounts but will also monitor their accounts to ensure that the merchants are making valid sales and not having issues that would jeopardize their accounts.

Support That Matches Business Risk

Small businesses will need support in the event of a problem: a batch that does not settle, a terminal that fails, a chargeback, funds that are held, or a gateway setting that is blocking sales. High-risk merchants may also experience support needs during underwriting reviews or when changing reserves and processors. The best provider will offer support to the business after approval, especially if the business is experiencing payment issues.

Q: What are merchant service providers?

A: Merchant service providers help small businesses accept and process payments, including credit cards, debit cards, ACH payments, ecommerce payments, invoices, and POS payments. These companies can offer payment gateways, payment-processing hardware, reporting, and fraud-detection software.

Q: What are the best merchant providers for small businesses?

A: The best merchant provider for your business will depend on your payment workflow. If you need high-risk payment support and consultant services, Payment Nerds might be the best provider for you. If you need something simple for in-person payments, Square might be best. For low-risk merchants who want to see all of the pricing up front, Helcim is a great provider. If you have an online business or developers building your products, Stripe is a great company to use. Finally, if you sell many products in person, Clover might be your best friend.

Q: What is the difference between a merchant account and a payment processor?

A: Both companies accept credit and debit card payments from customers. A merchant account is the underlying account that accepts the payments, while a payment processor handles the transaction between the two accounts. Some companies offer both services, while others may separate these entities.

Q: Do high-risk merchants need different merchant service providers?

A: Yes, high-risk merchants need providers that understand their unique underwriting and operational requirements. Mainstream merchants can approve small businesses quickly but reject merchants with high-risk categories.

Q: How should I compare merchant service provider pricing?

A: Compare the total cost of transaction processing. Check the rates for transaction fees, monthly fees, gateway fees, PCI fees, chargeback fees, hardware costs, keyed-entry fees, online payment fees, ACH fees, and reserves.

Q: Why does the Visa Acquirer Monitoring Program (VAMP) matter for my merchant service provider?

A: VAMP allows Visa to monitor fraud and chargeback activity for all merchants using their platforms. For online businesses with recurring or high-risk sales, monitoring chargebacks, fraud, and enumeration activity can help keep your business running smoothly while maintaining account stability.

Q: Can a small business switch merchant service providers?

A: Yes, they can switch providers, but must do so carefully. Small businesses should review their current merchant account provider to determine if switching will be challenging. Factors to consider include hardware compatibility, software integration, recurring payments, chargebacks, and account funding schedules.

Final Thoughts

There’s no such thing as the best merchant service provider for every business. For a brand-new company with low risks in how it accepts payments, a flat-rate merchant service provider may be the best solution. But a high-risk merchant services company may need something more flexible, with additional protections in place.

Payment Nerds can help small businesses and high-risk merchants to compare merchant service providers and identify which may work best for their unique business and payment models. For merchants, it’s not about finding a merchant service provider that just accepts their payments. It’s about ensuring their merchant service provider keeps their business approved and ready to grow.

Sources

- U.S. Small Business Administration Office of Advocacy. “Frequently Asked Questions About Small Business 2026.” Accessed June 2026.

- Visa. “Visa Acquirer Monitoring Program Fact Sheet.” Accessed June 2026.

- PCI Security Standards Council. “Merchant Resources.” Accessed June 2026.

- Helcim. “Save Money on Processing Fees.” Accessed June 2026.

- Square. “Processing Fees, Plans, and Software Pricing.” Accessed June 2026.

- Stripe. “Pricing & Fees.” Accessed June 2026.

- Clover. “POS System Pricing and Cost.” Accessed June 2026.

- Authorize.Net. “Plans and Pricing.” Accessed June 2026.

- PaymentCloud. “High-Risk Merchant Account.” Accessed June 2026.

- Durango Merchant Services. “High-Risk Payment Processing.” Accessed June 2026.