A Stripe or PayPal decline does not mean a business cannot accept payments. It can mean that the business model is not compliant with the payment platform’s policies.

A high-risk payment gateway will connect the business to the appropriate payment gateway, processor, and account, and ensure that fraud detection is in place – all prerequisites for surviving another account review…or avoiding a shutdown altogether.

Why High-Risk Merchants Need Specialized Gateway Solutions

High-risk merchants need specialized payment gateway solutions for several reasons. Depending on the type of business, the merchant account may need specific features such as the ability to perform recurring billing, store cards on file, process over-the-phone transactions, support multiple currencies, and include fraud detection and card testing software, as well as underwriting for the type of business.

While many gateway solutions allow merchants to quickly set up a business with a payment gateway, these solutions may not be ideal for high-risk merchants, as the gateway company may close the merchant’s account if it feels the merchant is violating its terms.

Why Stripe and PayPal Decline High-Risk Merchants

Before you apply elsewhere, understand why the business rejected you. The reason may be related to the types of products sold, chargebacks, high-ticket items, future deliveries, subscription models, regulated products, documentation requirements, or website claims.

While we may reject many applications, we do work with high-risk industries, including CBD products, travel, nutraceuticals, and digital products. Payment Nerds does not work with industries such as THC products and dispensaries, peptide merchants, research chemical merchants, counterfeit goods, gambling, and firearms sales without the proper license or for illegal activity.

Who Needs This High-Risk Payment Gateway Guide

This guide is useful for merchants that need more flexibility than a generic all-in-one platform provides.

It is especially relevant for:

- merchants dropped or declined by Stripe, PayPal, Square or Shopify Payments

- high-risk ecommerce merchants

- subscription, continuity and membership businesses

- CBD, vape, nutraceutical, adult, travel, dating and digital product merchants

- businesses with elevated chargebacks or fraud exposure

- merchants that need NMI, Authorize.net or another gateway connected to an approved merchant account

- operators comparing high risk payment processors

- merchants evaluating high risk merchant account providers

- businesses that need Visa Acquirer Monitoring Program (VAMP) visibility

If payment disruption would stop sales, delay fulfillment or freeze cash flow, gateway choice should be part of a larger account-stability strategy.

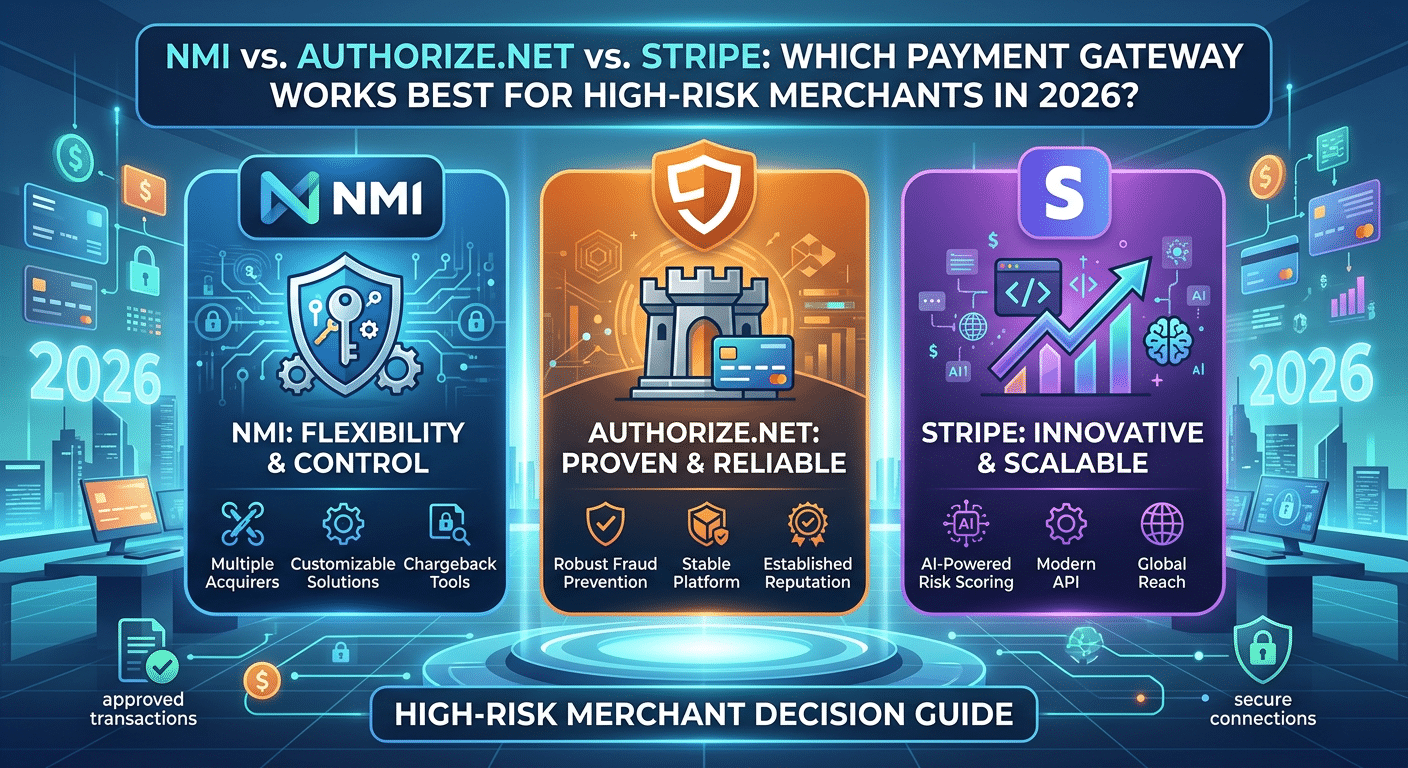

Best High-Risk Payment Gateway Options Compared

A high-risk merchant should compare gateways by processor compatibility, underwriting fit, fraud controls, reporting and chargeback workflows, not just checkout appearance.

| Gateway Option | Best For | Main Strength | Main Tradeoff |

|---|---|---|---|

| NMI | High-risk ecommerce, recurring billing, multi-MID and processor-flexible setups | Broad processor connectivity, gateway controls, recurring billing and fraud tools | Requires configuration and an approved merchant account |

| Authorize.net | Merchants that want a familiar gateway connected to merchant services | Strong name recognition, virtual terminal, eCheck and fraud tools | Underlying merchant account approval still matters |

| High-Risk Merchant Account + Gateway | Merchants declined by self-serve platforms | Better fit for underwriting, reserves, chargebacks and risk review | More documentation than instant onboarding |

| Payment Orchestration | Larger merchants using multiple processors, regions or brands | Routing flexibility and redundancy | Requires technical and operational maturity |

| Offshore Gateway Setup | Certain international or hard-to-place merchants | May provide options when domestic acquiring is limited | Higher scrutiny, cost and compliance complexity |

| ACH + Card Gateway | High-ticket, invoice-based and recurring merchants | Reduces reliance on cards while preserving card acceptance | ACH returns and authorization rules need monitoring |

| All-In-One Platform | Low-risk merchants that fit platform rules | Easy setup and clean user experience | Less flexible if the business becomes high risk |

The safest path is usually not to simply find another Stripe alternative. It is building a gateway and merchant account setup that matches the business model before transactions start running.

Best High-Risk Payment Processors and Gateway Setups Compared

Provider fit depends on the industry, processing history, chargebacks, product category, sales channel, ticket size, region and platform.

| Provider Or Setup | Best Fit For | Key Strength | Main Tradeoff |

| Payment Nerds | Merchants that need high-risk gateway strategy, merchant account guidance and processor-fit support after Stripe or PayPal says no | Connects gateway selection to underwriting, high risk payment processors, fraud tools, chargeback controls and Visa Acquirer Monitoring Program (VAMP) monitoring | More consultative than a self-serve payment app |

| NMI + High-Risk Merchant Account | Ecommerce, recurring billing and multi-MID merchants needing flexibility | Processor connectivity, reporting, tokenization, recurring billing and gateway control | Requires correct configuration and approved acquiring |

| Authorize.net + High-Risk Merchant Account | Merchants that want a familiar gateway with eCheck, virtual terminal and integrations | Recognized gateway, fraud tools, invoicing and merchant account compatibility | High-risk support depends on the merchant account provider |

| PaymentCloud | High-risk merchants needing application and placement support | Broad high-risk positioning and merchant account assistance | Pricing and reserves depend on underwriting |

| Durango Merchant Services | Hard-to-place, international or complex high-risk merchants | Experience with high-risk and offshore account placement | More specialized than many lower-risk merchants need |

| Easy Pay Direct | Ecommerce, continuity and high-risk merchants needing gateway strategy | High-risk account support and payment routing experience | Approval depends on category, history and processor match |

| SoarPay | High-risk and regulated merchants comparing account options | Industry-specific merchant account positioning | Terms vary by risk profile and documentation |

| Bankful | Ecommerce and Shopify merchants needing alternatives to standard processors | High-risk ecommerce and platform-oriented payment tools | Fit depends on product category and underwriting |

| Stripe | Supported ecommerce, SaaS and platform businesses | Strong APIs, checkout, billing and fraud tools | Not built for every restricted or high-risk category |

| PayPal | Low-risk merchants needing familiar checkout and wallet acceptance | Customer familiarity and easy checkout adoption | Acceptable use rules and account reviews may limit high-risk fit |

Payment Nerds is usually the strongest fit when the merchant needs help choosing between gateways, processors and high-risk merchant account providers rather than just opening another self-serve account. The best gateway setup should make the business more underwritable, not just easier to process for a few weeks.

How VAMP Impacts High-Risk Payment Processing

The Visa Acquirer Monitoring Program (VAMP) is the combined program for fraud and dispute monitoring. The VAMP ratio is the number of fraud reports and non-fraud disputes divided by the number of settled Visa transactions. TC40 is the number of Visa fraud reports, and TC15 is the number of Visa disputes.

The Visa Acquirer Monitoring Program (VAMP) is important for the selection of gateways because different gateways offer different levels of control of fraud and disputes. For instance, a gateway that cannot help to identify the source of fraudulent activity will leave a merchant reacting to a problem caused by their processor.

The Visa Acquirer Monitoring Program (VAMP) also includes enumeration monitoring. Enumeration attacks involve bots testing the cards on a checkout page. The enumeration ratio is the number of suspected card-testing attempts divided by the total number of authorization attempts over a given period. VAAI stands for Visa Account Attack Intelligence and is the score that Visa uses to identify enumeration attacks. If the enumeration ratio is at the Standard or Excessive level, the merchant will be warned and possibly charged fees for that period.

For high-risk merchants, the gateway should facilitate compliance with the Visa Acquirer Monitoring Program (VAMP) by monitoring indicators such as fraud and disputed transactions, fraud refund amounts, failed authorizations, and suspicious checkout activity.

Choosing the Right High-Risk Payment Gateway in 2026

Start with supportability. Ensure that your business and its operational elements will be approved by a bank that will open a merchant account with you. If your business is not suitable for a merchant account, then no payment gateway will work for you.

Review the features of the payment gateway companies. Consider whether they offer the specific features that your business requires. Look for features that indicate whether they are a suitable payment gateway for a high-risk business. Choose the one that will best help your high-risk account remain stable.

Understanding High-Risk Payment Gateway Costs

High-risk payment gateway costs typically include fees charged by the payment gateway company for services such as monthly payments, per-transaction payments, batch payments, account updater payments, fraud tool payments, ACH payments, chargeback payments, PCI payments, payment gateway setup fees, integration fees, and sometimes even chargeback alert programs.

High-risk payment processing can entail higher costs due to higher card rates, reserves, delayed card funding, and rolling reserves or volume limits for the merchant. Even if the payment gateway industry promises low fees, that will not help the merchant if the merchant account is unstable or does not support the types of sales this payment gateway supports.

Common High-Risk Payment Gateway Mistakes

The biggest mistake is assuming that using a gateway like NMI, Authorize.net, etc. is the same as having a high-risk transaction approved. You need an approved processor and merchant account to accept transactions.

Another mistake is hiding your real business model from Stripe and other payment processors that say no. Underwriters will look at your website, your products, your policies, your descriptors and your chargebacks. Being transparent about your business is the best way to get approved for a merchant account.

Key Features to Look for in a High-Risk Payment Gateway

Processor Compatibility

High-risk payment gateways must be compatible with the processor and merchant account that has approved the business. Approval of the payment gateway and the merchant account are not the same. NMI offers connectivity to many processors. Authorize.net works well with many merchant account providers. Either processor will work with a merchant account that has approved the business.

Fraud And Card-Testing Controls

High-risk payment gateways must offer tools to prevent fraud and chargebacks. Fraud rules include AVS, CVV, velocity, IP filters, 3DS, risk scoring and device signals. For online merchants, card testing is crucial. It is necessary to prevent bots from using the checkout form to test stolen credit card data.

Recurring Billing And Card-on-File Support

Most high-risk merchants use recurring billing and card-on-file software. These software programs allow merchants to store customer data so that they can accept payments without asking for the card every time. Recurring billing software must be easy to understand by customers. If customers are confused about the renewal of their subscription, this can contribute to chargebacks for that product or service.

Virtual Terminal And MOTO Tools

Some merchants will require a virtual terminal or MOTO program. A virtual terminal allows merchants to enter card information over the phone. MOTO transactions do not require a card to be presented to the merchant. Documentation is required for the sale.

Chargeback And VAMP Reporting

A high-risk payment gateway should offer chargeback and VAMP reports for merchants to review chargebacks, refunds, declines, failed transactions, chargeback alerts and fraud reports. These reports should be detailed enough to provide insight into which product is causing most of the chargebacks for the merchant. For merchants enrolled in the Visa Acquirer Monitoring Program (VAMP), having insight into chargebacks and fraud is required before the acquiring bank decides that the merchant is engaging in high-risk behavior.

Ecommerce And Software Integrations

Many high-risk merchants use ecommerce software and other software programs in their management. These software programs can include WooCommerce, Shopify (third-party gateways only), BigCommerce, Magento, customer relationship management (CRM) software, subscription software and accounting software. A payment gateway that does not integrate well with these programs will cause problems with chargebacks and refunds for the merchant. The merchant will not be able to see which software is causing the issues.

FAQs About High-Risk Payment Gateways

Q: What is a high-risk payment gateway?

A: A high-risk payment gateway is a payment gateway set up for merchants who need more flexibility and control over fraud controls, processor compatibility, and underwriting support. The merchant must have an approved merchant account or processor behind the gateway.

Q: Why do Stripe and PayPal say no to some merchants?

A: Companies like Stripe and PayPal may not allow certain merchants due to the type of products or services they offer, chargebacks, or risk factors associated with the business. This could mean that the merchant will need to use a high-risk payment processing solution to manage their transactions.

Q: What are high-risk payment processors?

A: High-risk payment processors will work with merchants who are likely to have high rates of chargebacks, fraud issues, high ticket sizes, or regulatory issues. These processors will require merchants to undergo underwriting to determine whether they can take on the risks associated with these types of merchants.

Q: What are high-risk merchant account providers?

A: High-risk merchant account providers will work with merchants who want to set up payment processing in categories that standard merchant account providers may not allow. These companies will look at your industry, documentation, chargeback history, business model, reserves, and the merchant gateway and processor you use.

Q: Is NMI a high-risk payment gateway?

A: NMI is a flexible payment gateway that many merchants in high-risk categories use. All that is required is that the merchant has an approved merchant account and a processor behind the gateway.

Q: Can Authorize.net work for high-risk merchants?

A: Authorize.net can work for high-risk merchants, but only if you have a merchant account provider that will work for your high-risk merchant account and category.

Q: Should high-risk merchants use offshore gateways?

A: Offshore gateways are used for high-risk merchants who may have difficulty placing themselves under a domestic payment gateway. The issue with offshore merchants is that there are usually higher costs and greater risk associated with their payment gateway providers. It is best to consider domestic options first.

Q: Can Payment Nerds help high-risk merchants after Stripe and PayPal say no?

A: If Stripe and PayPal have said no to your high-risk merchant application, Payment Nerds can help compare different payment gateways, high-risk payment processors, high-risk merchant account providers, fraud tools, and VAMP programs to find the best solution for your high-risk business and products.

Conclusion

If Stripe and PayPal say no, that does not necessarily mean another payment processor can help you.

High-risk merchants require a payment gateway solution that connects their merchant account to their payment processor, fraud and chargeback reporting software, and their ecommerce website.

Payment Nerds can assist high-risk merchants in comparing available payment gateways and processing solutions, including various payment processors, merchant accounts, NMI, Authorize.net, ACH, and VAMP solutions. Our payment processing consultants aim to restore your merchant account access and provide a solution that delivers long-term stability.

Sources

- NMI. “Secure Payment Gateway & Processing Solutions.” Accessed June 2026.

- NMI. “Payment Gateway.” Accessed June 2026.

- NMI. “Partner Training: Multi-MIDs & Agent Set-Up.” Accessed June 2026.

- Authorize.net. “Credit Card Payment Processor, Online Payments Systems and Processing.” Accessed June 2026.

- Authorize.net. “Plans and Pricing.” Accessed June 2026.

- Authorize.net. “Fraud Prevention, Detection and Protection.” Accessed June 2026.

- Stripe. “Prohibited and Restricted Businesses.” Accessed June 2026.

- Stripe. “High-Risk Merchant Accounts Explained.” Accessed June 2026.

- PayPal. “Acceptable Use Policy.” Accessed June 2026.

- PayPal Help Center. “What Is PayPal’s Acceptable Use Policy?” Accessed June 2026.

- Visa. “Visa Acquirer Monitoring Program Fact Sheet.” Accessed June 2026.

- PCI Security Standards Council. “Merchant Resources.” Accessed June 2026.